Europe’s LeaderSHIP 2020 strategy to increase the competitiveness of European maritime technology is the result of a close co-operation between the industry, the trade unions, maritime regions, Member States and the European Commission. The European ships and maritime equipment industry employs more than 500,000 people and has an average annual turnover of around €72bn but faces strong competition, and, like many other industries, the effects of an unprecedented crisis.

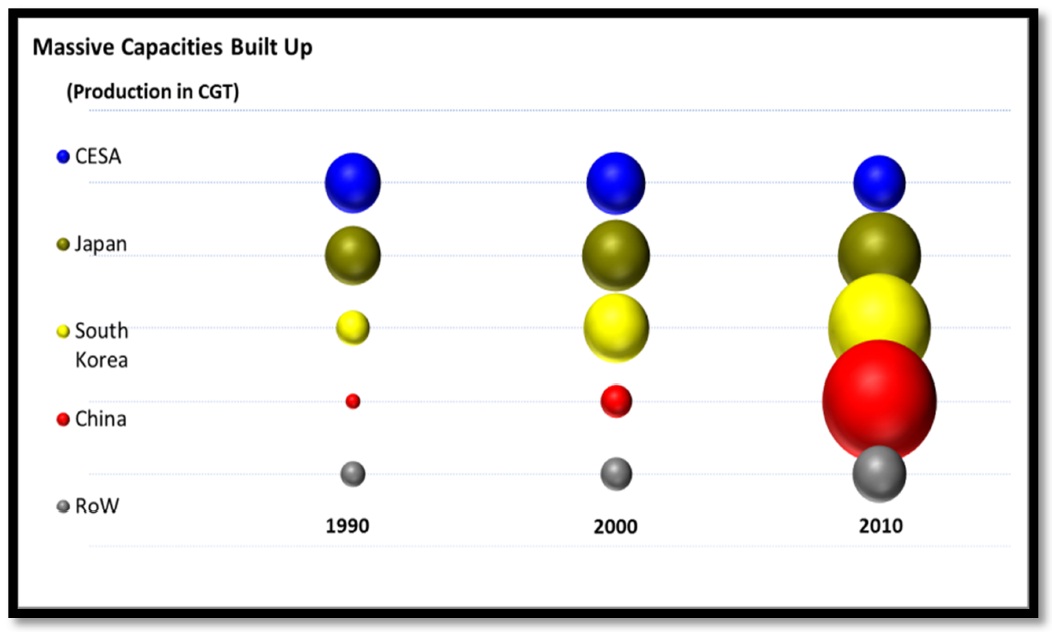

During the last decade the construction of cargo ships has largely shifted to China, Korea and Japan producing four-fifths of the world’s vessels. European production has mainly focused on the production of specialised high-tech ship types.

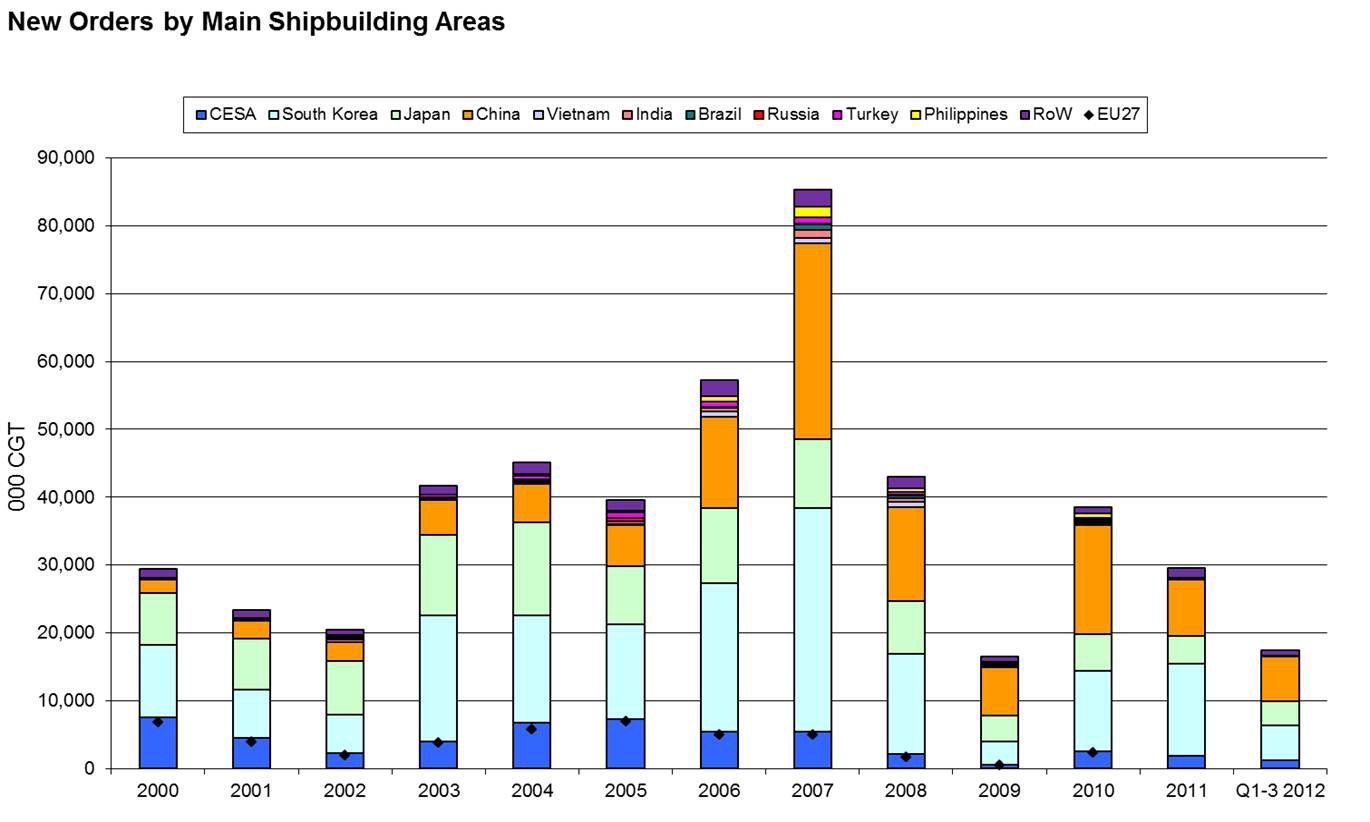

New orders for ships have virtually collapsed from a pre-crisis speculative boom of 85mln cgt to 16 mln cgt in 2009 and have remained low. The expected average order volume is 30-40m cgt annually. At the same time the expanded global shipyard capacity reached new output records year on year peaking in 2012 at around 60m cgt. The capacity expansion in shipbuilding has mainly taken place in China, Korea and other emerging markets, however Europe has refrained from taking this approach. The long production cycle in shipbuilding means that the impact of low orders on the supply chain and on employment is only now being felt. This is particularly concerning for Europe.

The LeaderSHIP 2020 strategy’s recommendations range from the wider use of EU instruments to foster new skills, competence and qualifications, to Public Private Partnerships for new maritime research, European Investment Bank (EIB) funding opportunities and smart specialisation strategies in regional policy. The new strategy provides a series of recommendations for the short and medium term, to support sustainable growth, high value jobs and address the societal challenges that the shipbuilding and maritime industry currently faces.

The report proposes actions in four main areas:

Employment and skills: The strategy underlines the problem of skills shortages for the sector and proposes a systematic approach at EU level to map the available skills and to address skill and training needs, through the use of EU programmes. Member States and Regions should also be involved, especially through the creation of regional networks. LeaderSHIP 2020 also calls for the effective communication of the long term vision of the maritime industries. Existing tools provided by EU programmes and initiatives should be harnessed to promote the attractive image of a career in the European maritime technology industry. Finally, the strategy recommends the promotion of mobility and the exploration of ways to harmonise degrees and accreditation systems in the EU, to meet market needs and improve graduate employability.

Improving market access and fair market conditions: These actions involve international organisations i.e. OECD, WTO and ILO, on IP rights and public procurement. They focus on:

- The need to redefine the role of the OECD Working Party on shipbuilding, in order to consider new ways to regulate unfair and unsustainable market practices. This should include monitoring of government interventions and price developments. New methods to reduce capacity and overhaul common rules should also be explored.

- Designing a broad framework and strategy to include ‘public values targets’ in European public tenders as well as higher levels of innovation, and enforcing greater reciprocity in market opening between the EU and non-EU countries.

Access to finance: Access to finance has become the single most important factor in competing for international shipbuilding contracts. Methods to address issues in access to finance, financing environmental improvements and diversification into new markets include:

- Making best use of the EIB funding opportunities and possibilities for broadening its lending activities, primarily for projects related to green shipping, offshore renewable energy, and retrofitting.

- Exploring the opportunity of a potential measure for long term ship financing by the European Commission, Member States, financial operators and the maritime technology industry.

- Finally, on the possibility to create a Blue “Private Public partnership” (PPP), the strategy calls for the industry to examine the possibility of a ‘blue’ PPP in the light of the European industry structure and respecting state aid rules.

Research, development and innovation: LeaderSHIP 2020 suggests that industry develops a roadmap for a PPP at EU level (Horizon 2020) to focus maritime research on zero emission and energy efficient vessels and towards zero technical accident vessels as well as emerging market opportunities. The feasibility of a PPP on marine renewable energy could also be explored. The possibility of allocating structural funds 2014-2020 for the diversification of the maritime technology industry into new market sectorsshould be explored by Member States and coastal regions, especially in the context of regional strategies for smart specialisation.

The LeaderSHIP 2020 initiative builds on the LeaderSHIP 2015 strategy published in 2003 – which emphasised competitiveness, innovation and specialisation in suitable market segments. Compared to the previous strategy, LeaderSHIP 2020 involves a broadened range of actors: all maritime technology industries and representatives of their clients such as the wind energy industry, the shipowners and the dredging industry. EU Regions were also very much involved in the process and particular attention was given to the potential of “smart specialisation”.

The European shipbuilding and maritime equipment industries consist of:

- Shipbuilding and ship repair: The European shipbuilding industry and ship repair industry is made up of around 300 yards of which more than 80% can be considered to be ‘small to medium’ (building ships of 60-150mt). The remaining yards can be defined as ‘large’. Around 90% of the order book is for export markets.

- Marine equipment manufacturing: The European marine equipment manufacturing and industry (propulsion, cargo handling, communication, automation, integrated systems, etc.) is made up of around 7,500 companies, the vast majority of which can be considered to be ‘small to medium’. Around 70% of production is for export markets.

Source: European Commission

I am a European seafarer working at sea for the some money and the same food as the unqualified guys from some Asian low-cost countries ! Do you think that somebody care about that ?! I do not think so !